U.S. Economy This Week: So Much Good News the Media Are Going to Get Tired of Hiding It

Even with the 2017 tax cut extension still not enacted, the administration's move toward market-affirming policies and away from progressive tax-spend-debt madness is paying dividends.

Guest post by economist Robert Genetski, Ph.D.

Unlock exclusive financial insights and expert analysis to navigate market trends and make informed investment decisions: subscribe@classicalprinciples.com.

Friday’s report on spending, incomes and inflation going into the second quarter shows the economy doing well. Spending is rising at close to a 5 percent annual rate, real growth and inflation is in the 1 percent to 2 percent vicinity going into the second quarter. Despite all the noise associated with tariffs, the overall trends continue to move in a positive direction.

Thursday’s first quarter GDP report shows current dollar spending and incomes were up at only a 3½ percent annual rate. Year-over-year current dollar GDP has declined to 4.7 percent, from 5.7 percent a year ago. The first quarter slowdown helps to contain inflation for the rest of this year.

New orders for durable goods in April declined sharply. The March surge was likely due to avoiding tariffs. Even so, the average of orders in March and April was up 5 percent from the average for January and February. Hence, second quarter new orders are off to a strong start.

This week’s data begins arriving tomorrow, with the May business surveys for manufacturing companies and then on Wednesday for service companies. The previously reported advance S&P survey for early May points to an improvement in

manufacturing to break-even (50) and an improvement in service company performance from break-even to 52.

Expect both the ISM and S&P surveys for May to show business activity above break-even.

Also on Wednesday, April new orders for manufacturing should show a pattern similar to that of durable goods orders: down sharply for the month, but up for the average of April and May.

Wednesday’s ADP jobs data for May also will provide advance insight into the economy. We expect a gain of 70,000 jobs, up from 62,000 in April.

Friday’s May employment report is expected to show a gain of 125,000 private payroll jobs, down from 167,000 reported in April.

The judicial decision to sideline Trump’s tariffs was postponed. The initial ruling was that the President lacked the authority to impose such tariffs. The higher court’s decision allows the tariffs to be implemented pending further appeals.

Even if the Supreme Court rules the president lacks tariff authority, he has other options. The President can ask Congress for the authority to impose tariffs or use other means to pressure foreign countries to accept his terms.

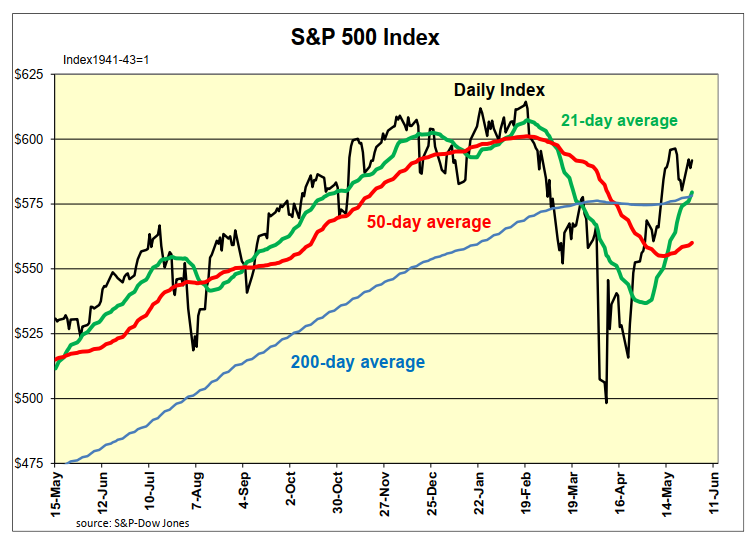

The modest reaction in stocks to the initial announcement suggests little has changed with respect to current policy.