There Is No Possible Bailout for the Federal Government

Even the U.S. economy, the best in the world, cannot support this much government debt, let alone what is projected for the next ten years. The numbers are frightening.

With federal government debt projected to rise from the current $36.9 trillion to $54.4 trillion in 2034, the upward pressure on interest rates is sure to collapse the economy, greatly reduce federal tax revenues, and bring on defaults on government debt, Social Security, and Medicare, plus an inability to fund other entitlements, defense, and everything else the government does, sometime in the intervening years.

A household or business facing such a dire prospect would immediately take measures to avert it, including spending less, earning more if possible, and selling off assets, to pay down the debt; the alternative being bankruptcy (and the loss of those very assets). The U.S. government, by contrast, has always been able to rely on the American people and the great engine of growth that is the free-enterprise system to create a big enough pie from which to take its slice.

The government long ago became extremely comfortable with the fact that the American people have always been able to bail them out. Bailouts, however, notoriously lead to further bailouts and then to bankruptcies. It is a simple moral hazard: the unmatched prosperity-generating ability of America’s free-enterprise system tempts members of the government to think that they can dream as big as they want in their quest to buy votes. That was exactly what we experienced in 2021 through 2024.

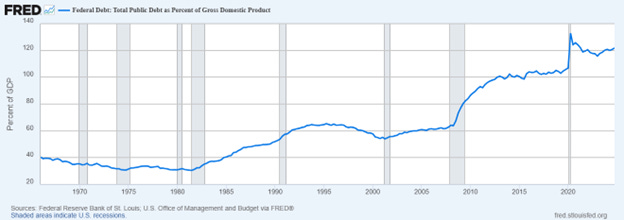

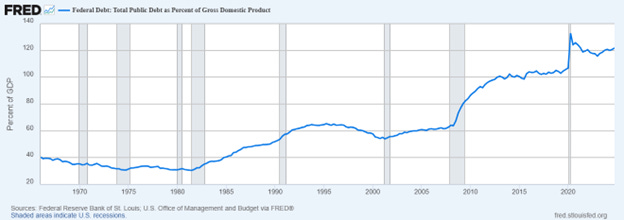

As a result, we are rapidly reaching the limits of even the great American economy to fund government greed and overreach. The public has been hit from both ends: the government encourages consumption by overspending and suppresses production by overtaxing and overregulating. Here is what that looks like (skip past these charts if you have just eaten):

If the federal government were to come to its senses, it would start by cutting spending (by at least $2 trillion per year) and increasing revenues (by lowering tax rates and reducing regulation). We’ve seen how willing Congress has been to do that. Failing that, selling assets remains the other major option.

Unfortunately, that would not raise much money. “The federal government owns roughly 640 million acres, about 28% of the 2.27 billion acres of land in the United States,” the Congressional Research Service reported in 2020. Land and transportation policy analyst Randal O’Toole estimated at that time that selling all (politically) possible federal lands and the oil, natural gas, and coal on them would bring in at most $3.7 trillion. That would cover at most 14 percent of the 2020 federal debt, and we’re on track to add another $30 trillion to that in the next decade, more than doubling the debt.

In addition to land and the resources on it, the Federal Reserve estimates the national government’s other assets are worth $9.29 trillion. Of course, many of those assets are probably not in a sellable condition or things that anybody would want at the estimated price.

The $13 trillion that we would hope to raise by selling all those properties would not even pay for all the debt scheduled to be added between now and 2034, falling $4.5 trillion short. In addition, selling all that property would be a one-time deal, so the $13 trillion debt reduction would not be repeatable later if (when) the government goes on its merry way imagining that the American people are an unlimited source of tax money.

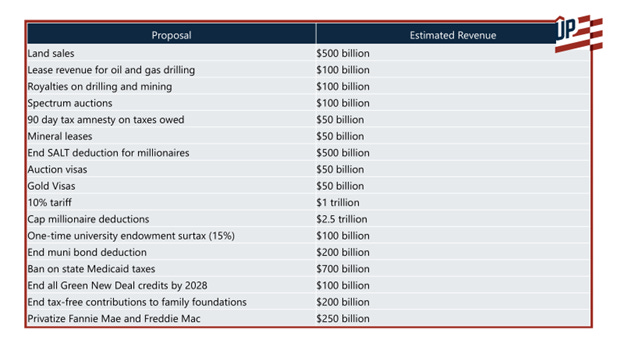

Perhaps in recognition that the government’s assets won’t get us very far, The Committee to Unleash Prosperity (CTUP) suggests a smaller land sale and additional measures to pay for more cuts to tax rates, totaling $6.55 trillion:

CTUP’s plan seems to recognize that major spending cuts are not a possibility and that the federal debt has already become so gargantuan that only rapid economic growth can possibly put off a crisis, by reducing the annual federal deficit below projections over the next decade. That is probably true. Instead of paying down the debt, CTUP proposes to stop adding to it, which would indeed be an improvement though not a solution.

Unfortunately, even that is exceedingly unlikely. The opposition party and the nation’s press and other institutions would immediately condemn any plan to implement CTUP’s suggested changes as a sell-off of the American people’s precious assets to pay for a massive tax cut for the rich.

I do not see any politically plausible scenario in which the U.S. government averts a fiscal crisis and default on the debt, with ensuing social chaos, in the coming years. Looking at all the numbers, the only real solution is obvious: pray for a miracle.

Ugh, we're doomed.

Given these projections, what specific policies or reforms do you think could realistically gain bipartisan support to start addressing the debt issue before it reaches a crisis point?