Dow 40,000, Common Sense 0

Stock markets have been rising for a variety of reasons, not all of them good.

The Dow Jones Industrial Average surpassed a major milestone two weeks ago, rising above 40,000 on Thursday before sliding back down to 39,869, and going up again above 40,000 for Friday’s close.

That represents a 40 percent increase over the stock market’s September 2022 recent low. This week, all three slid back a bit, but they all rose significantly overall in May.

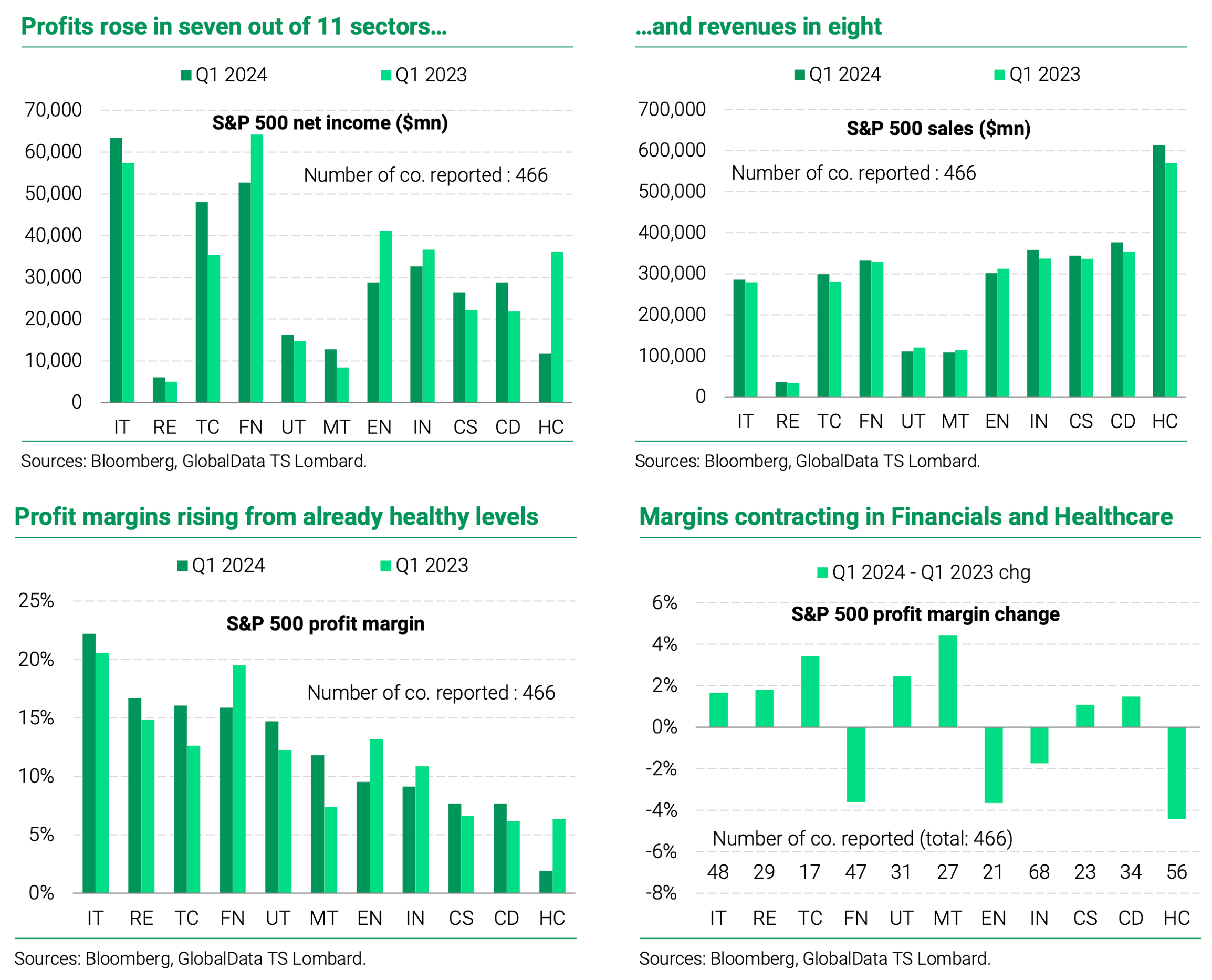

Part of the explanation is that profits are up:

{kind=link}

Source: Andrea Cicione - TS Lombard

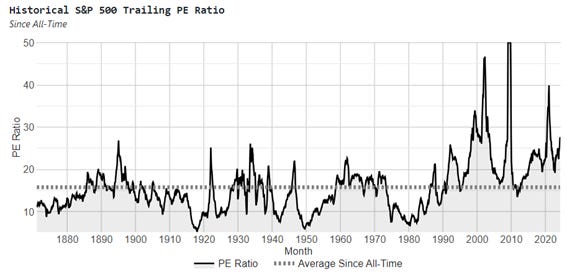

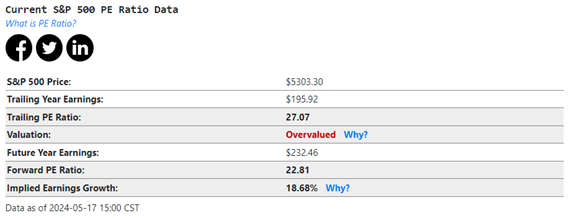

One might well argue, however, that price/earnings ratios are too high at present, as the following charts suggest:

Source: Stock Market PE Ratio

But OK, we’ll leave that aside and grant that the recent rise in profits makes stocks more attractive. Why are profits up? Let’s examine some things about the overall economy.

Side note: I am on the record as saying, “This economy does not look good,” as recently as three weeks ago (Life, Liberty, Property #59). That might seem a bit dumb now, but I’m not so sure.

The Dow appears to be anticipating an easing up on money tightening by the Federal Reserve (Fed). The Wall Street Journal reports,

Data Wednesday showed that core consumer prices, which exclude the volatile categories of food and energy, last month posted their smallest increase since April 2021. The Dow climbed after the inflation report and then crossed 40000 Thursday before paring its gains.

Clearly, investors are thinking that the slight slowing of inflation in April means the Fed will soon relent on its tightening of the money supply via higher interest rates and reductions of its holdings of federal government bonds. Conventional (i.e., Keynesian) thinking is that the reduction of interest rates will allow the economy to expand more rapidly (by making it less-expensive to borrow for consumer spending and business investment).

The increase in interest rates in the past two years has not hurt the economy, it would seem: “Yet interest rates remain much higher than in the years before the pandemic,” the WSJ reports. “The yield on the benchmark 10-year Treasury topped 5% in October for the first time in 16 years. It has since fallen to 4.376%, still more than double its 1.909% level at the end of 2019.”

Thus, “the recession predicted by so many economists hasn’t materialized, giving investors hope that stocks might keep climbing,” the WSJ reports. “‘Not only didn’t we have a recession, we had a robust economy with tight labor markets, healthy consumers who were consuming,’ said Katie Nixon, chief investment officer for Northern Trust Wealth Management.”

As the quote from Nixon indicates, U.S. economic growth has been driven by expansive consumer spending since 2021, surprising those who thought that the interest rate increases would bring on a recession. This demand-driven expansion might cause some to agree with a phrase often misattributed to another Nixon (the economy-destroying President Richard Nixon): “We are all Keynesians now.”

I have a different theory: Could it be that the ongoing increase in housing prices is helping to spur this consumer spending? Not exclusively, of course, but as a big contributing factor? (This increase in housing prices, by the way, is mainly a result of overall price inflation plus governments’ suppression of housing construction plus immigration increasing the demand for housing.)

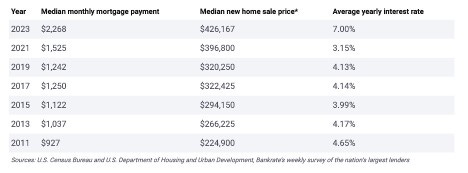

House prices and mortgage payments have risen rapidly in recent years, especially since 2020:

Source: Regime Critic

People are reluctant to sell their houses given the costs of buying another, and that reluctance cuts the supply of houses available to buyers, which contributes to further price hikes for the houses that do go on the market. Meanwhile, interest rates have risen, as noted above. That adds more to the cost of a new house.

As a result, the median monthly mortgage payment for a new house is almost double what it was in 2019.

Median household income rose by 17.8 percent between 2019 and January 2024 (from $65,712 to $77,397). The median sales price for a new home in the United States rose by more than double that: 39 percent (from $310,600 to $430,700). (Note: in April, the median price hit a new record high, at $433,558, raising the increase to 40 percent. That is a 6.2 percent rise year-over-year.)

The median monthly payment for a home purchase was $2,775 in the four weeks ended April 14, The Wall Street Journal reports. In 2019 it was $1,242. That means the percentage of the median household income required to pay the mortgage on the median-priced house rose from 22.7 percent in 2019 to 43 percent today. That is a truly awful number.

Home equity accounted for 65 percent of Americans’ household wealth in 2021. According to Federal Reserve numbers, U.S. homeowners in 2019 had a median net worth of $293,900, whereas renters’ median net worth was just $7,230. That means homeowners had more than 40 times the wealth of renters.

On paper, that is. You have to live somewhere, so if you sell your increasingly valuable house, you have to buy … some other increasingly valuable house.

As a result, the housing supply is “historically low,” according to RedFin. “Homeowners who would like to move are staying put so they can hold on to their lower-rate mortgages,” the WSJ reports in its story on the Dow record. “The resulting lack of homes for sale has pushed prices beyond the reach of many prospective buyers.”

If you do not move, however, the rise in the value of your house increases the amount of money you can borrow against your rising home equity.

It makes sense that a simultaneous increase in house valuations and inability to sell one’s home would funnel money toward other purchases and investments. If people are not buying new homes, they have more ready cash to spend on other things—a lot more than in previous years, in fact, given the rise of homeowners’ equity as the calculated values of houses rise.

Thus the U.S. economy has been expanding via a rapid increase in household borrowing, which has fueled increases in consumer spending, pushing up prices of services in particular. These are price hikes, not wealth increases.

A rising Dow and expanded household borrowing make great sense in this context of rising housing values. These are increases in spending, however, not necessarily indicative of rises in the real value of goods and services. As Josiah Lippincott notes at his Regime Critic Substack:

The cost of food, housing, and transportation have nearly doubled in the last five years. In effect, the value of the starting salary for new college graduates has fallen by almost half. The median new college graduate salary today is the equivalent of making $12 an hour in 2019.

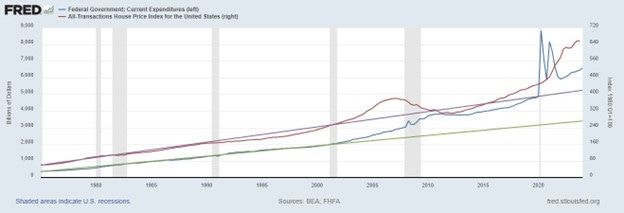

As I have noted regularly in this newsletter and elsewhere, federal government overspending fuels inflation. Here’s a little graph I made that shows how the rise in federal spending compares with the rise in housing prices:

Note the two trendlines: green for the 1970-2000 trend in federal spending, and purple for the trend in the housing price index for those years. Federal spending moves above trend in 2000 and much above trend in 2021. Housing prices move above trend in 2000, and much above trend in 2021.

That is no coincidence. The increase in housing prices is being caused by more than a rise in the quality of housing—the latter does contribute over time, but not over the course of two or three years. The price increases track well with federal spending because the latter is increasingly funded by deficits, which create inflation via Fed monetization of the increasing federal debt.

Meanwhile, real (inflation-adjusted) stockholder wealth has risen to 10 times its value of four decades ago, the Committee to Unleash Prosperity (CTUP) reports.

That is real monetary wealth, in the sense of being inflation-adjusted, but does it represent greater real value of goods and services across the economy? Not since 2021, it doesn’t. Whereas “the vast majority of the gains from the past four-decade-long bull market from—Reagan through the Trump presidency—were REAL gains, not inflationary gains,” CTUP notes in another article, “about 80% of the stock rise during Biden's tenure has been phantom gains due to inflation.” CTUP’s chart illustrates this increasing gap:

Source: Committee to Unleash Prosperity

Given these factors, the recent rise of the Dow does not appear to be indicative of a great increase in the real value of goods and services produced in the United States.

In addition, “these illusionary gains are subject to taxes since capital gains aren’t indexed to inflation.” Naturally, then, as part of President Joe Biden’s campaign to intensify the excessive deficit spending and overregulation that have created this Potemkin economy, the administration wants to increase capital gains taxes radically. Biden proposes a near-doubling of the percentage taken from high-income taxpayers with long-term gains—to 39.6 percent from the current 20 percent—and more than double for some taxpayers, who will pay 44.6 percent.

(Of course, they won’t really pay this, as I noted in Life, Liberty, Property #58. It is all a circus show designed to get suckers to vote for Democrats and Rinos. The latter label applies to nearly all Republicans, alas.)

In summary, the federal government’s economic destruction is real, ongoing, and intensifying.

So, congratulations to those of my readers who have lots of money invested in Dow stocks. I am truly happy for you.

Overall, however, I’ll say it again:

This economy does not look good.