History suggests that the Fed’s loosening of the money supply may be arriving too late to prevent an eventual downturn caused by the massive overspending imposed by Biden and Harris.

The Federal Reserve finally decided to cut interest rates last Wednesday, by one-half of a percentage point. Markets greeted the long-expected move toward looser money with initial enthusiasm and then “sobered up a touch,” as The Wall Street Journal described it.

The markets would do well to stay sober. The interest rate cut does not have the power to undo the damage the Biden-Harris fiscal fiasco has done to the nation’s economy.

Fed Chair Jerome Powell emphasized his belief that the economy is in good shape, in a press conference last Wednesday announcing the rate cut. “The U.S. economy is basically fine,” Powell said. “Our intention is really to maintain the strength that we currently see in the U.S. economy.”

Last Tuesday’s report from the U.S. Census Bureau on household income, poverty, and health care in 2023 indicates otherwise. Workers are receiving lower pay after inflation, and the losses have been worst for lower-income workers. “Real median earnings for full-time workers last year declined 1.6% and even more for high-school grads (3.3%),” The Wall Street Journalreports. “This means inflation outpaced wage gains for most low-wage workers.”

American households are struggling financially in the Biden-Harris economy. Real median household income is lower than it was in 2019 and has improved little since January 2021, the Census data show. In fact, among whites, Asians, and Hispanics, real median income grew by 10 times as much under President Donald Trump as it did during the Biden-Harris administration, and blacks’ median income growth under Trump was more than double the Biden-Harris amount, economist Larry Kudlow noted on Fox Business News.

Today’s baby step by the Fed is too little, too late. Correcting the August CPI for Owners' Equivalent Rent (OER) bias reduces [the] 12 month inflation rate from 2.5% to just 1.4%. By not switching to lower rates a year ago, the Fed has damaged bank balance sheets and shut down bank loans. Small businesses and their employees are paying the price.

Rutledge’s contention is that the consumer price index (CPI) is inaccurate because of the inclusion of OER (which no one actually pays and is essentially imaginary) as a large factor, and it has been showing much greater overall price inflation than what people have been experiencing in the past couple of years. (See Rutledge’s article for his explanation of the OER effect.)

“They should have pushed rates down a year ago; rates today should be 3%, not 5%,” Rutledge writes. “Their inaction has already damaged the economy.”

Thanks for reading Life, Liberty, Property! Subscribe for free to receive new posts and support my work.

The Fed’s over-extension of its tight-money policy is beginning to bring on a credit crunch, Rutledge argues:

Small businesses depend on bank loans for the working capital they need to meet payroll and pay other costs before they get paid, in turn, by their customers. In normal times, lending decisions are based upon interest rates, fees, and credit quality of the customers, and bank loans grow in line with GDP. On occasion, however, something goes wrong with bank balance sheets, banks shut down lending, and we go through a period of non-price rationing. The newspapers call it a credit crunch.

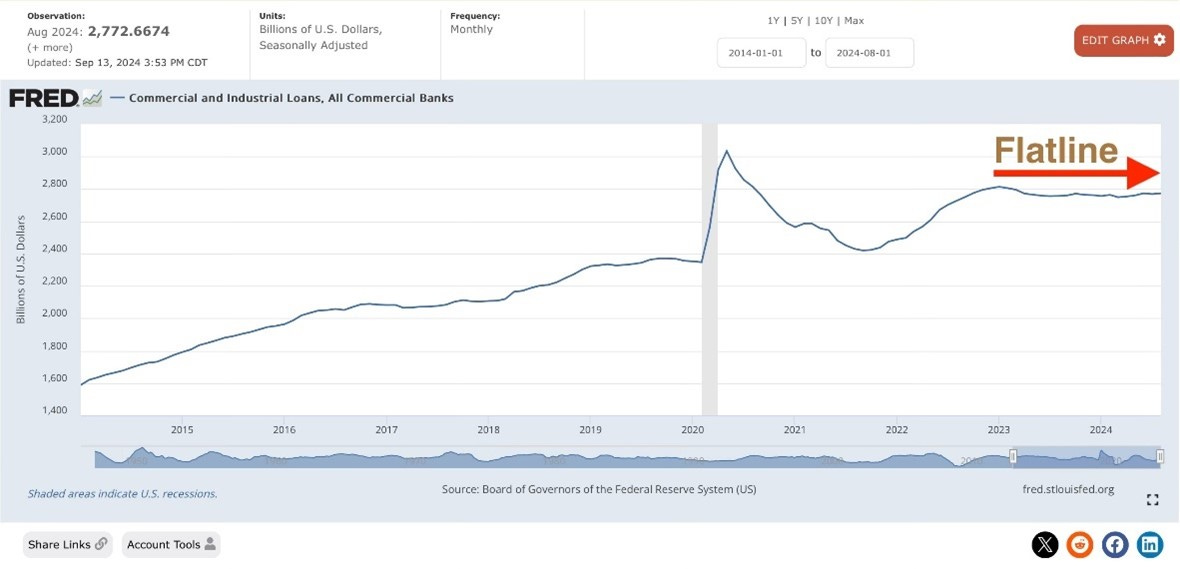

As you can see in the chart, above, we have a baby credit crunch brewing today. After their wild ride during the COVID pandemic, business loans resumed their normal course until they flatlined in January, 2023, just before the Silicon Valley Bank bust.

In fact, the total outstanding stock of bank commercial and industrial loans ($2779 billion) today is $34 billion lower than it was in January, 2023 ($2813 billion). That means, over the past 20 months, banks have collected $34 billion more from their customers than they have loaned to their customers, not including payments for interest and fees!

Problems for businesses are tragedies for workers. Rutledge writes,

In August, ADP reported that private employers added only 99,000 employees. … Small businesses with 20-49 employees—the ones that depend on bank loans to meet payroll—reduced employment by 12,000 people.

The flatlining of business loans has been caused by “the damage done to the values of the Treasury bonds and mortgage securities on regional bank balance sheets when the Fed jacked up interest rates to current levels,” Rutledge writes.

The credit crunch “is a mild one so far,” especially when compared with the subprime mortgage crisis of October 2008 to October 2010, Rutledge observes. It could get much worse, however, Rutledge argues:

Where it goes from here will depend on what the Fed does with interest rates. If they quickly bring rates down, regional bank balance sheets will improve and banks will sooner or later start lending again. If the Fed continues to drag its feet, business loans will decline and the economy will deteriorate.

Regular readers of this site know that I agree with Rutledge about the effect of OER in distorting the reported inflation rate and that the Fed has been keeping money too tight for too long. Now, six weeks away from a presidential election, the Fed suddenly decides to loosen the money supply. One might be forgiven for being suspicious about that. As David Stockman writes, “Everything the Fed does, in fact, is grounded in the statist politics of the Keynesian model. There is no economic science about it.”

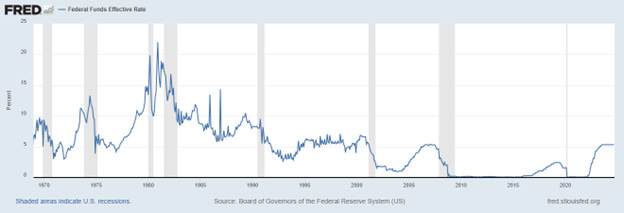

As the following chart shows, the Fed generally starts reducing interest rates before a recession hits (shaded areas), and then continues the rate cuts during the downturn:

Two facts: we are not in a recession (as far as we know at present), and the Fed has begun cutting rates and indicates it will cut further in the coming months.

I believe that Rutledge’s assessment of inflation and the Fed’s reaction is accurate. As Rutledge notes and history suggests, the Fed’s loosening of the money supply may be arriving too late to prevent an eventual downturn caused by the massive overspending imposed by Biden and Harris.

Thanks for reading Life, Liberty, Property! This post is free to all. Please share it widely.

I think I've seen perhaps one article which mentioned the before or after rate . It's a necessary piece of information . Dropping half a point to ~ 4.75% is very different than dropping half a point from 1% to 0.5% .

I think I've seen perhaps one article which mentioned the before or after rate . It's a necessary piece of information . Dropping half a point to ~ 4.75% is very different than dropping half a point from 1% to 0.5% .